Blue Book

- 1 -

Amendment B: Repeal the

Gallagher Amendment

Amendment B proposes amending the Colorado Constitution to: 1

• repeal the Gallagher Amendment requiring residential and nonresidential2

property tax revenues to make up the same portion of total statewide property3

taxes as when the Gallagher Amendment was adopted in 1982, including t

he4

r

equirement that sets the nonresidential assessment rate at 29 percent.5

6

What Your Vote Means 7

A “yes” vote repeals

sections of the Colorado

Constitution that set a

fixed statewide ratio for residential and

nonresidential property tax revenue.

Assessment rates for all property types

will remain the same as they are now,

projected future decreases in the

residential assessment rate will not be

required, and any future increases in

assessment rates would require a vote of

the people.

A “no” vote leaves

constitutional provisions

related to property taxes in

place, maintaining current requirements

for setting the assessment rates used to

calculate property taxes. This is

expected to result in a decreasing

residential assessment rate over time

and in automatic local mill levy increases

in jurisdictions where required by law.

NO

YES

Blue Book

- 2 -

Summary and Analysis for Amendment B 1

In Colorado, property taxes fund local government services, including services 2

provided by cities, counties, and special districts, such as local police and fire 3

protection, hospitals, transportation, and the local share of K-12 education. The 4

Gallagher Amendment sets statewide rules for property taxes funding these local 5

services. This analysis first summarizes what Amendment B does, then describes 6

how property taxes are calculated, and finally discusses how the measure affects 7

taxpayers and governments. 8

What does Amendment B do? 9

Amendment B removes provisions related to the residential and nonresidential 10

assessment rates from the constitution, including the provisions commonly known as 11

the Gallagher Amendment. 12

The Gallagher Amendment currently requires that residential and nonresidential 13

property make up constant portions of total statewide taxable property over time. 14

Since adoption in 1982, these provisions have required that the taxable value of 15

residential property make up about 45 percent, and the taxable value of 16

nonresidential property about 55 percent of statewide taxable property. Actual 17

property values have not matched the required ratios over time because residential 18

property values have generally grown faster than nonresidential property values. 19

Since the taxable portion of most nonresidential property values is fixed at 20

29 percent, the state legislature adjusts the residential assessment rate to maintain 21

the required ratio, as shown in Figure 1. 22

Amendment B removes these provisions from the constitution, leaving the residential 23

and nonresidential assessment rates at their current rates in state statute. Under 24

current law, the residential assessment rate is expected to decrease in future years, 25

reducing the amount of property taxes paid by property owners and collected by local 26

governments. Amendment B would eliminate automatic tax increases adopted by 27

some local jurisdictions to offset revenue losses from the Gallagher Amendment. In 28

jurisdictions that have not adopted automatic tax increases, Amendment B eliminates 29

projected future decreases in the residential assessment rate and any increase in 30

nonresidential or residential assessment rates would require voter approval. 31

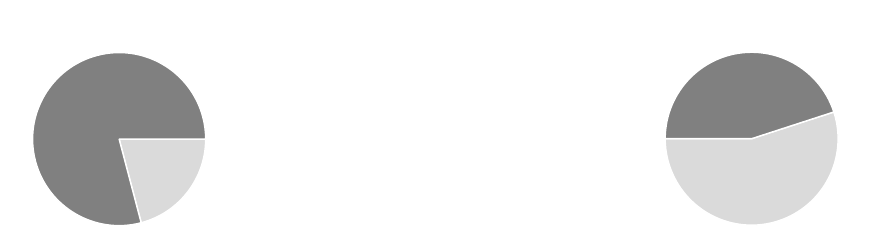

Figure 1. Assessment Rate Adjustments Under Current Law 32

* Actual property values are for 2019. The residential assessment rate is for 2019 and 2020. This

33

assessment rate has fallen over time to maintain the fixed ratio for taxable values of about 45 percent34

residential and 55 percent nonresidential.35

** Assessment rate for most nonresidential property.36

7.15% Residential Rate*

The legislature adjusts the residential

assessment rate to achieve the

required ratio for taxable values.

Fixed 29% Nonresidential Rate**

Actual Property Values* x Assessment Rates = Taxable Values

Residential

45%

Nonresidential

55%

Residential

80%

Nonresidential

20%

Blue Book

- 3 -

How are property taxes calculated? 1

Property taxes are paid by residential homeowners and nonresidential property 2

owners, including farmers, ranchers, oil and gas operators, and other businesses. 3

Property taxes are paid on a portion of a property’s actual value. The actual value of 4

property is determined by the county assessor or state property tax administrator. 5

The portion of the actual value on which taxes are paid is known as taxable value. 6

Taxable value is also known as assessed value. 7

Taxable value is calculated by multiplying the actual value by an assessment rate. 8

The assessment rate is currently 7.15 percent for residential properties and is fixed 9

at 29 percent for most nonresidential properties. Mines and lands that produce oil 10

and gas are assessed at different rates than other nonresidential property. 11

Taxable value is then multiplied by the tax rate, called a mill levy, to determine the 12

property taxes owed. One mill equals $1 for each $1,000 dollars of taxable value. 13

For example, 100 mills is equal to a tax rate of 0.1 (100/1,000), or 10 percent. The 14

tax rate varies for each property based on the local taxing districts in which it is 15

located. Figure 2 provides an example of how property taxes are calculated. 16

17

Figure 2. Property Tax Calculation 18

Example: Property valued at $300,000 and taxed at 100 mills 19

Taxable value = Property value x Assessment rate

Residential $300,000 x 7.15% = $21,450 taxable value

Nonresidential $300,000 x 29% = $87,000 taxable value

Property taxes = Taxable value x Tax rate (Mills/1000)

Residential $21,450 x 0.100 = $2,145 owed

Nonresidential $87,000 x 0.100 = $8,700 owed

20

How has the residential assessment rate changed over time? 21

In most years, residential property values have grown faster than nonresidential 22

values, causing the residential assessment rate to be lowered so that residential 23

properties continue to make up about 45 percent of statewide taxable value. As 24

shown in Figure 3, the residential assessment rate has been reduced from 25

21 percent when these provisions went into effect in 1983 to a current rate of 26

7.15 percent. With the fixed nonresidential assessment rate at 29 percent, and the 27

current 7.15 percent residential assessment rate, nonresidential property owners pay 28

an effective tax rate that is approximately four times higher than residential property 29

owners. The downward shift of the residential assessment rate is expected to 30

continue in future years. 31

Blue Book

- 4 -

Figure 3. Gap in Assessment Rates Since 1983 1

When nonresidential property values grow faster than residential property values, the 2

residential assessment rate must increase to maintain the constant ratio; however, 3

other constitutional provisions require that voters approve such an increase. As a 4

result, the state legislature may decrease, hold flat, or ask voters to approve an 5

increase in the residential assessment rate. Since 1999, there have been 6

six instances when the residential assessment rate would have increased, but the 7

legislature did not refer a measure to voters and the rate instead stayed flat. 8

What factors impact property taxes? 9

Property taxes paid by a property owner are dependent on three components: actual 10

property value, the applicable assessment rate, and the mill levy. Changes to any of 11

these components impact the amount of property taxes paid and thus, the amount of 12

revenue collected by a local government. Amendment B concerns only residential 13

and nonresidential assessment rates; however, other changes to property values or 14

tax rates also impact the amount of property taxes owed. 15

What are the automatic mill levy increases that some local governments have 16

adopted? 17

In response to the shift between residential and nonresidential assessment rates, 18

many local governments have adopted laws that automatically increase local mill 19

levies to offset the revenue losses from the Gallagher Amendment. These automatic 20

increases counteract the reduction in the residential assessment rate and result in a 21

net property tax increase for nonresidential property owners. These automatic mill 22

levy increases would not be triggered if Amendment B passes. 23

How does Amendment B affect residential property taxpayers? 24

Under Amendment B, the residential assessment rate will remain at the current 25

7.15 percent for residential property. Without the measure, the residential 26

assessment rate is projected to decrease in future years due to the relative growth of 27

7.15%

21.85%

29%

0%

5%

10%

15%

20%

25%

30%

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Residential

Assessment Rate

Gap Between Nonresidential and

Residential Assessment Rates

Nonresidential

Assessment Rate

Tax Year

Blue Book

- 5 -

residential property values compared to nonresidential property values. As a result, 1

Amendment B is expected to eliminate projected future reductions in the residential 2

assessment rate, and thus, could result in higher property taxes paid by residential 3

taxpayers, if property values increase and if automatic mill levy increases do not 4

offset assessment rate reductions. 5

How does Amendment B affect nonresidential taxpayers? 6

Under Amendment B, the assessment rate will remain in state law at 29 percent for 7

most nonresidential property. Amendment B will have no impact on the amount of 8

taxes paid by most nonresidential property owners. 9

In the local governments that have approved automatic mill levy increases to offset 10

revenue reductions from the Gallagher Amendment, Amendment B will prevent 11

property tax increases for businesses, farmers, and other nonresidential property 12

owners, as the higher mill levies that would have been triggered by decreases in the 13

residential assessment rate under the Gallagher Amendment will no longer be 14

required. 15

How does Amendment B impact local government revenue? 16

Under the current system, the decline in the residential assessment rate has 17

constrained property tax revenue to local governments. The impact varies across 18

the state, with the largest impacts occurring in areas without much nonresidential 19

property or with only slow growth in home prices. These areas are generally small 20

and rural; however, metropolitan areas with slow growth in home values are also 21

impacted. Amendment B prevents further decreases in the residential assessment 22

rate, thus preventing declines in local government property tax revenue used to 23

provide local services. 24

How does Amendment B impact state government spending for schools? 25

Schools are funded through a combination of state and local revenue, with the state 26

making up the difference between an amount of school district funding identified 27

through a formula in state law and the amount of local tax revenue generated. By 28

preventing future decreases in the residential assessment rate, Amendment B 29

increases local property tax collections for school districts and reduces the amount 30

the state must pay to make up the difference. 31

If Amendment B passes, can the state legislature change the assessment rates? 32

Under Amendment B, the state legislature may decrease the assessment rates, but 33

cannot increase them without voter approval. Currently, assessment rates are set in 34

state law at 7.15 percent for residential property and 29 percent for most 35

nonresidential property. 36

For information on those issue committees that support or oppose the

measures on the ballot at the November 3, 2020

, election, go to the

Colorado Secretary of State’s elections center web site hyperlink for ballot

and initiative information:

h

ttp://www.sos.state.co.us/pubs/elections/Initiatives/InitiativesHome.html

Blue Book

- 6 -

Arguments For Amendment B 1

1) The Gallagher Amendment is outdated and full of unintended consequences. If2

the Gallagher Amendment is not repealed, owners of high-end homes i

n3

D

enver’s wealthiest neighborhoods would get a tax cut next year, while small4

businesses and farmers would pay a larger share of property taxes. Th

e5

G

allagher Amendment causes small businesses to be taxed at a rate four time

s6

hi

gher than residential property owners, and penalizes rural and low incom

e7

c

ommunities that lack a significant commercial tax base.8

2) Colorado has some of the lowest residential property taxes in the nation,

and9

A

mendment B fixes property tax assessment rates at their current levels.10

Amendment B is not a tax increase. Under Amendment B, the property tax rates11

homeowners and businesses pay could only be increased by a vote of the12

people.13

3) Amendment B will prevent deep cuts to schools, hospitals, fire protection,

and14

other local services in many areas of the state. Declines in the residential15

assessment rate caused by the Gallagher Amendment have resulted in16

significant reductions in vital services provided by local governments, particularly17

in rural and low income communities. Amendment B allows local governments t

o18

continue providing services that their communities expect

.19

Arguments Against Amendment B 20

1) Amendment B results in higher property taxes for homeowners by preventi

ng21

future drops in the residential assessment rate. Increasing home values hav

e22

already resulted in higher property taxes for many homeowners. Higher taxes23

mean that homeowners will have less money to spend or save, and landlords24

may increase rents, at a time when many are already struggling to make ends25

meet

.26

2) The current property tax system keeps residential property taxes low, and27

prevents special interests from obtaining tax breaks at the expense of28

homeowners. Amendment B removes an important protection for homeowners29

from the constitution. Without these protections, homeowners may end u

p30

paying an increasing share of property taxes.31

3) There are better alternatives to amending the constitution. Local governments32

can instead ask their voters to raise tax rates or seek other solutions to provi

de33

services such as fire protection, schools, and libraries. These alternatives woul

d34

allow voters in each local jurisdiction to decide for themselves how to best fund35

services for their community

.36

Estimate of Fiscal Impact for Amendment B 37

Local revenue and spending. For many local governments, including counties, 38

cities, school districts, and special districts, Amendment B will result in increased 39

property tax revenue. The amount of any increase will depend on what the 40

residential assessment rate would have been in the future without the measure, as 41

well as whether voters have already approved local tax increases to counteract 42

future potential decreases in the residential assessment rate. 43

State spending. To the extent that Amendment B increases property tax revenue to 44

school districts, additional funding will be available for the local share of the state’s 45

system of school finance, reducing the amount the state must pay to make up the 46

Blue Book

- 7 -

difference between local revenue and the school district funding amount identified 1

through a formula in state law. 2

Taxpayer impacts. Maintaining the current residential assessment rate results in 3

higher property taxes for many residential property owners compared to what they 4

would owe if residential assessment rates were lowered in the future. The impact on 5

property owners from holding the residential assessment rate constant in the future 6

will vary based on several factors, including what future decreases in the residential 7

assessment rate would have been required without the measure, the actual value of 8

the property, and the tax rates of the local taxing districts. The measure does not 9

impact the assessment rate for most nonresidential taxpayers. 10